Carbon Farming: From Shared Vision to Real-World Scale

Marie-Lou Manca; Oleksandra Kvasnytska; Marja Roitto

Sustainability Expert; Market and Customer Research Specialist; Research Coordinator

Published

7 April 2026

Climate Reality Europe Cannot Ignore. The urgency is undeniable. Europe is now the fastest-warming continent, and in 2024, we crossed the +1.5°C threshold. Current trajectories point toward a potential +4°C increase by the end of the century, a scenario widely considered unlivable.

But beyond climate, the risks are systemic. Up to 60% of European food and agri-food systems are at risk in the coming decades, with 70–85% currently uninsured. Agriculture sits at the center of this challenge. It accounts for around 10% of EU emissions, while simultaneously being one of the sectors most exposed to climate change impacts. Food systems also contribute to broader planetary pressures, from biodiversity loss to water scarcity. By 2030, global freshwater demand is expected to exceed supply by 40%.

Against this backdrop, carbon farming is gaining traction.

We recently attended the 3rd European Carbon Farming Summit (Padua, Italy, March 2026), a gathering that brought together farmers, corporates, policymakers, researchers, and platforms around a shared ambition: scaling carbon farming across Europe.

What stood out immediately was the strong sense of alignment. Across sessions, stakeholders largely agreed on both the urgency and the direction of travel. Yet, despite this consensus, one question kept surfacing:

If we all agree on the challenges, why are we not moving faster?

Carbon as a Catalyst, Not a Commodity

A recurring idea throughout the summit was that carbon should not be seen as a commodity, but as a catalyst. Carbon acts as a proxy for the regenerative capacity of land. It provides a measurable entry point into broader environmental outcomes, biodiversity, soil health, water systems. This reinforces the need for a landscape approach, where carbon and biodiversity are treated as complementary rather than separate objectives.

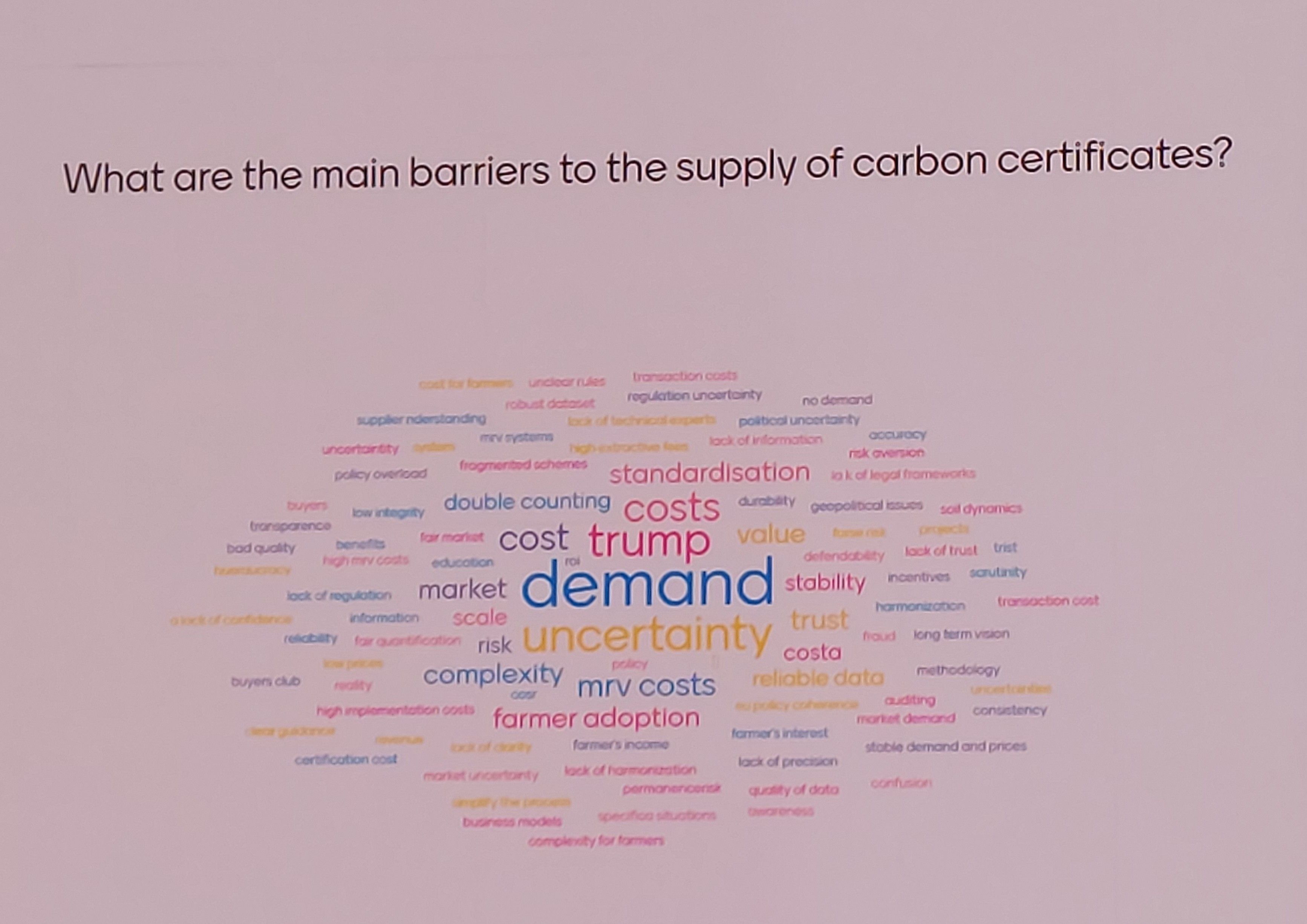

A Market Full of Potential, Yet Not Scaling

There is no doubt that the opportunity is real. Major players such as BASF, Bayer, KPMG, and leading food companies are investing in carbon farming. Business cases are emerging, with prices for these large players set around €70–80 per tonne seen as viable. Farmers themselves are interested, especially when practices improve the resilience of their land. And yet, the market is not scaling.

Demand Remains the Core Bottleneck

The issue is not supply: it is demand. • Demand for credits remains unstable and uncertain • Voluntary markets are not delivering at scale • Companies struggle with Scope 3 accounting, which represents up to 98% of agrifood emissions • As a result, many shift toward external carbon removals rather than investing in their own value chains Without predictable demand, farmers cannot justify the risk of transition.

Complexity Is Slowing Everything Down

The second major barrier is system complexity. • Multiple standards and certification frameworks • Repeated data collection across systems • Complex value chains with low traceability In some cases, the same data is collected multiple times for different crops and buyers, creating a heavy administrative burden. Technically, solutions exist. But the lack of harmonization and interoperability prevents scaling.

Farmers Carry the Risk

At the center of this system are farmers, and today, they carry a disproportionate share of the risk. Transitioning practices require upfront investment, long-term commitment without guaranteed return. For many small farms, this creates a “wait-to-profit” risk they simply cannot afford. At the same time, the value of these efforts is often misunderstood. Profit does not only come from new revenue streams like carbon credits,it can also come from reduced costs, such as lower fertilizer use and more efficient production systems.

Beyond economics, farmers are driven by deeper motivations: a commitment to passing on healthy land (over carbon metrics) to the next generation and a long-term vision of resilience.

Yet they face real challenges:

• Lack of access to technical knowledge

• Carbon markets perceived as too complex, too early, too expensive

• “Tidy field” mindset clashing with regenerative farming realities

• A growing generational gap (only ~12% of EU farmers are under 40)

And still, when incentives are clear and fair: farmers engage.

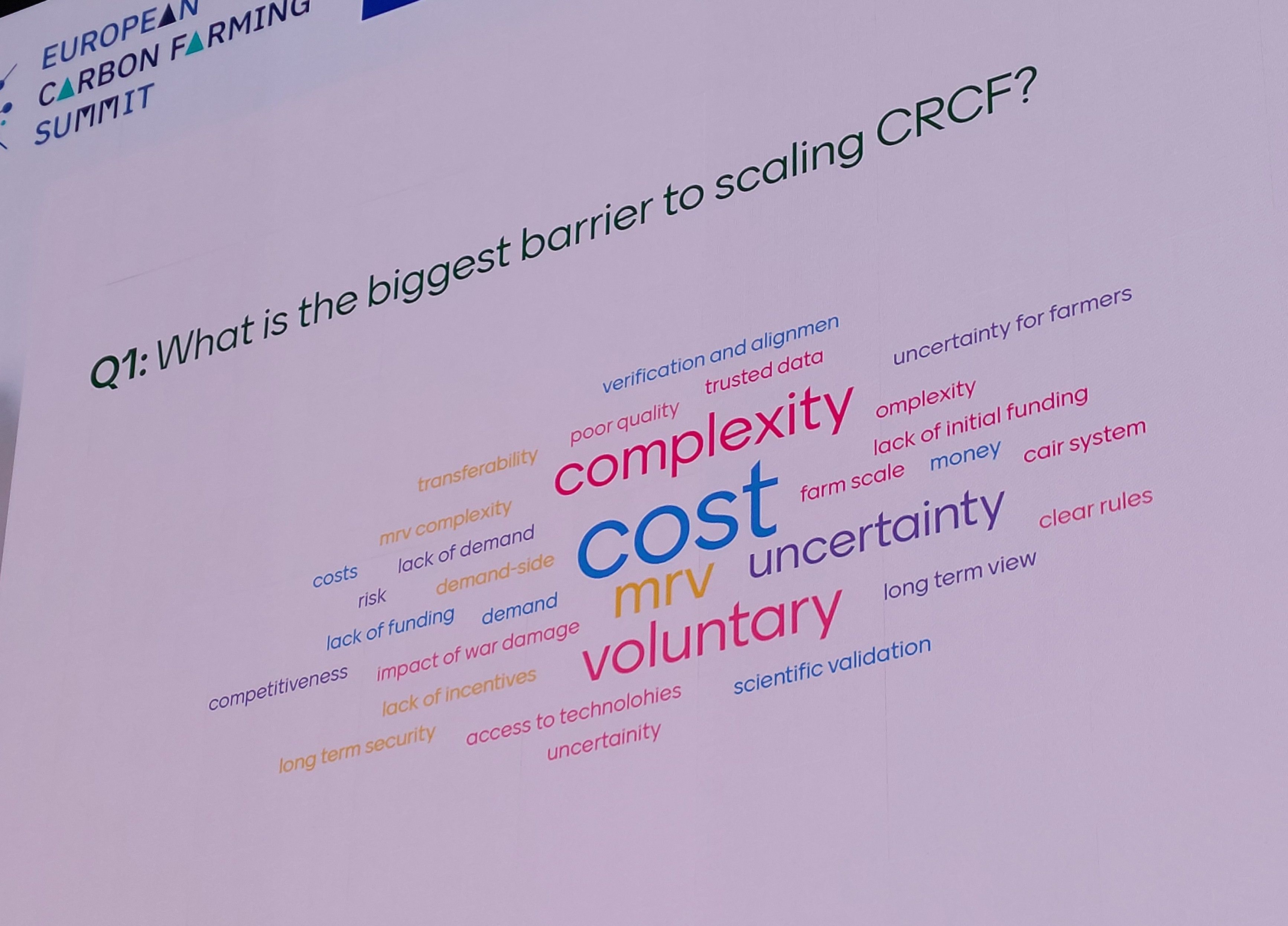

From Fragmentation to System Change

Incremental fixes will not be enough. What is needed is system-level change.

1. Build Stable Demand • Long-term offtake agreements • Buyer clubs aggregating public and private demand • Stronger policy-driven demand

2. Simplify and Harmonize • Align methodologies and standards • Develop shared EU data infrastructure • Enable interoperability between tools The objective is clear: reduce friction and ease the burden on farmers.

3. Rethink Financing Farmers need a financing stack, combining: • Public funding • Private investment • Banking and insurance There is also a need to balance paying for practices vs. outcomes, given the long timelines of environmental impact.

4. Build Trust Through Credibility

Trust depends on:

• Robust certification frameworks (e.g., CRCF)

• Clear rules on Scope 3 accounting and co-claiming across value chains

• Transparent methodologies and Monitoring, Reporting, Verifying (MRV) s ystems

Trust is local, peer-to-peer. Without trust, there is no demand, there is no offer: there is no market.

The EU’s Role: From Regulator to System Builder

The EU has a critical role to play, not just as a regulator, but as a system builder.

This includes: 1) Connecting supply and demand, 2) Providing shared infrastructure, 3) Aligning policies such as CAP and CRCF and 4) Ensuring farmers are represented in governance.

Today’s landscape is rich but fragmented. Unlocking scale will require alignment.

Beyond Carbon: Acting Now, Not Waiting for Perfection

A variety of credits is emerging, including carbon, biodiversity, water, and broader nature or landscape-based credits, reflecting a more holistic view of land stewardship. Within this landscape, social and community-based credits go beyond environmental impact to recognize contributions such as fair labor practices, improved working conditions, rural livelihoods, and community resilience. While still less mature and more difficult to standardize, they highlight an essential dimension of the transition: ensuring that sustainability efforts deliver tangible benefits for the people behind the land, not just the ecosystems themselves.

While attention is expanding toward biodiversity and nature credits, the message was clear: We cannot wait for perfect frameworks to act.

Carbon provides a starting point, unlocking investment now while building the foundation for broader environmental markets.

Alignment Is There -Acceleration Is Not (Yet)

A key paradox emerged: We all recognize the challenges. We largely agree on the solutions. And yet, large-scale action remains limited. At the same time, the growing involvement of major corporates confirms that a real business case exists. The missing piece remains: unlocking demand at scale.

What Comes Next: From Discussion to Action

As part of this year’s summit, we also hosted a workshop together with our partners in the PATH2CC project (Pathways to Carbon Credits for Small Farms in Europe). This session focused on one of the most critical challenges discussed throughout the event: how to make carbon markets accessible, viable, and attractive for small farms across Europe. The discussions highlighted key barriers, from demand uncertainty and data complexity to cost structures and knowledge gaps, and explored how to better connect farmers, buyers, and policymakers in a workable system. We will be sharing dedicated insights from this workshop in an upcoming article on the blog. Stay tuned, and if you’re interested in exploring collaboration opportunities around carbon farming and small farm inclusion, please reach out via the form below.

Get in touch to discuss your goals with our experts

©2026 COVERE², All rights reserved